STRONGSVILLE, Ohio — Strongsville-based Union Home Mortgage has announced an unspecified number of layoffs this week, joining the roster of other large mortgage lenders in recent days that have reduced their workforces amid declining volume in new applications for mortgages and refinances.

Cindy Flynn, the chief marketing and communications officer at Union Home Mortgage, said the company is “temporary adjusting [its] staffing levels” amid the quickly shifting residential housing market, which is due in large part to a historically low number of homes for sale, inflation as well as increasing interest rates. It is unclear how many staffers were let go; the company has not filed a WARN notice with the Ohio Department of Jobs and Family Services.

“Like other companies in our industry, "Union Home Mortgage is temporarily adjusting staffing levels to accommodate rapidly changing marketplace conditions and business needs,” Flynn said in a statement. “We remain confident in continuing to be one of the fastest growing independent mortgage bank lenders in the country and providing a world-class culture and the highest quality of customer service.”

The layoffs at the once rapidly growing mortgage lender follow similar job reductions this week at other big name lenders, including Rocket Mortgage and Wells Fargo. However, industry experts said the job losses aren’t terribly surprising, considering the monumental increase over the past two years in the number of people working for mortgage lenders.

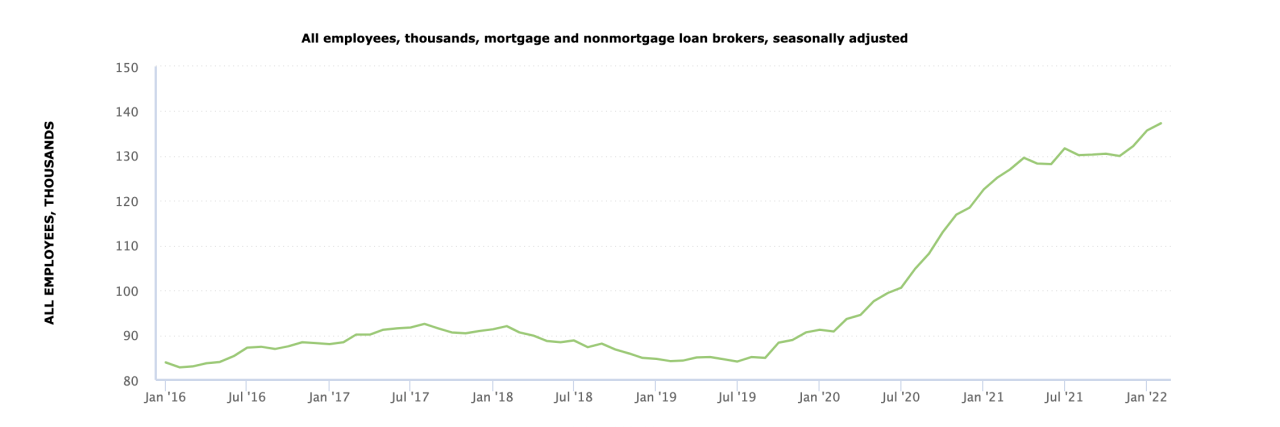

According to the Bureau of Labor Statistics, total employment in the lending industry has increased by more than 60 percent since July 2019 from 84,000 total workers nationwide to more than 137,000. The hiring spree, experts said, was in response to the white-hot housing market that followed the initial lockdowns during the COVID-19 pandemic.

However, with the Federal Reserve increasing interest rates earlier this year and more rate increases expected throughout 2022, demand for new mortgages as well as chronically low inventory in the housing market has fallen precipitously.

“The spike in mortgage rates over the past month as the Fed has looked to curb inflation is really freezing activity in the housing market,” said Michael Goldberg, an associate professor and executive director at Case Western Reserve University’s Veale Institute for Entrepreneurship. “It has slowed down new buying activity. It has slowed down refinancing and, thus, the larger mortgage lenders are responding by laying off staff.”

Coinciding with the interest rate hikes has been a significant decrease in applications to refinance mortgages has been nearly cut in half over the past six months, according to the Mortgage Banker’s Association.

According to research from Realtor.com, the impact of the interest rate hikes is only just beginning to impact the housing market.

“The combination of more sellers listing homes for sale and fewer home buyers able to contend with today’s high costs will lead to growth in the number of homes on the market in the months ahead,” said Danielle Hale, the chief economist at Realtor.com. “This reality should help tame price growth as more options and fewer competitors enable buyers to be choosier. Sellers who want to capture the largest possible buyer audience for their home would be well served to list sooner rather than later. Buyers who can still afford to continue shopping should reassess their target home search price to make sure it’s been adjusted to account for the budget impact of today’s much higher mortgage rates.”

The transitory state of the housing market comes as consumers are grappling with inflation levels at a 40-year high. Inflation, coupled with higher borrowing costs for both new home purchases as well as credit card debt, will likely leave consumers with a discernible decrease in purchasing power.

As for the employees affected by the layoffs at Union Home Mortgage, Goldberg said those looking for new employment are still at an advantage considering the tight labor market.

“It still is a very frothy labor market and there are lots of opportunities. It might be different than not necessarily walking down the street from one mortgage company to the next; it could be a different industry,” Goldberg said. “It could be outside of Cleveland but maybe staying right here in Northeast Ohio and doing it remotely. Many of us have lived through these downturns and upturns but it has been a very challenging — and confusing for many people — two years.”